{kind=link}

Whenever you join with Betterment, you possibly can arrange funding objectives you want to save in direction of. You possibly can arrange numerous funding objectives. Whereas creating a brand new funding objective, we’ll ask you for the anticipated time horizon of that objective, and to pick one of many following objective sorts.

- Main Buy

- Training

- Retirement

- Retirement Earnings

- Basic Investing

- Emergency Fund

Betterment additionally permits customers to create money objectives via the Money Reserve providing, and crypto objectives via the Crypto ETF portfolio. These objective sorts are outdoors the scope of this allocation recommendation methodology.

For all investing objectives (apart from Emergency Funds) the anticipated time horizon and the objective kind you choose inform Betterment while you plan to make use of the cash, and the way you intend to withdraw the funds (i.e. full speedy liquidation for a serious buy, or partial periodic liquidations for retirement). Emergency Funds, by definition, do not need an anticipated time horizon (while you arrange your objective, Betterment will assume a time horizon for Emergency Funds to assist inform saving and deposit recommendation, however you possibly can edit this, and it doesn’t influence our really helpful funding allocation). It is because we can not predict when an sudden emergency expense will come up, or how a lot it is going to price.

For all objectives (apart from Emergency Funds) Betterment will suggest an funding allocation based mostly on the time horizon and objective kind you choose. Betterment develops the really helpful funding allocation by projecting a variety of market outcomes and averaging the best-performing danger stage throughout the Fifth-Fiftieth percentiles. For Emergency Funds, Betterment’s really helpful funding allocation is shaped by figuring out the most secure allocation that seeks to match or simply beat inflation.

Beneath are the ranges of really helpful funding allocations for every objective kind.

| Aim Kind | Most Aggressive Really useful Allocation | Most Conservative Really useful Allocation |

|---|---|---|

| Main Buy | 90% shares (33+ years) | 0% shares (time horizon reached) |

| Training | 90% shares (33+ years) | 0% shares (time horizon reached) |

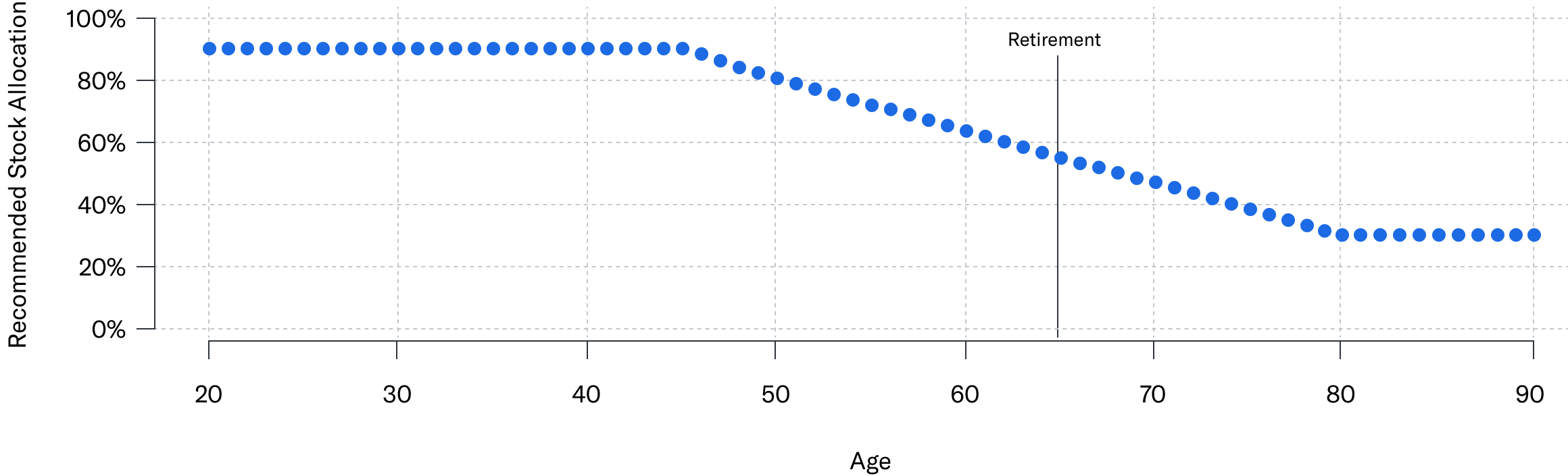

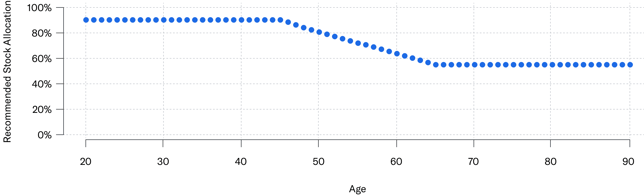

| Retirement | 90% shares (20+ years till retirement age) | 56% shares (retirement age reached) |

| Retirement Earnings | 56% shares (24+ years remaining life expectancy) | 30% shares (9 years or much less remaining life expectancy) |

| Basic Investing | 90% shares (20+ years) | 56% shares (time horizon reached) |

| Emergency Fund | Most secure allocation that seeks to match or simply beat inflation | Most secure allocation that seeks to match or simply beat inflation |

As you possibly can see from the desk above, usually, the longer a objective’s time horizon, the extra aggressive Betterment’s really helpful allocation. And the shorter a objective’s time horizon, the extra conservative Betterment’s really helpful allocation. This leads to what we name a “glidepath” which is how our really helpful allocation for a given objective kind adjusts over time.

Beneath are the complete glidepaths when relevant to the objective sorts Betterment presents.

Main Buy/Training Targets

Retirement/Retirement Earnings Targets

Determine above exhibits a hypothetical instance of a shopper who lives till they’re 90 years outdated. It doesn’t characterize precise shopper efficiency and isn’t indicative of future outcomes. Precise outcomes could fluctuate based mostly on quite a lot of elements, together with however not restricted to shopper modifications contained in the account and market fluctuation.

Determine above exhibits a hypothetical instance of a shopper who lives till they’re 90 years outdated. It doesn’t characterize precise shopper efficiency and isn’t indicative of future outcomes. Precise outcomes could fluctuate based mostly on quite a lot of elements, together with however not restricted to shopper modifications contained in the account and market fluctuation.

Basic Investing Targets

Betterment presents an “auto-adjust” characteristic that can mechanically modify your objective’s allocation to manage danger for relevant objective sorts, turning into extra conservative as you close to the top of your objectives’ investing timeline. We make incremental modifications to your danger stage, making a easy glidepath.

Since Betterment adjusts the really helpful allocation and portfolio weights of the glidepath based mostly in your particular objectives and time horizons, you’ll discover that “Main Buy” objectives take a extra conservative path in comparison with a Retirement or Basic Investing glidepath. It takes a close to zero danger for very quick time horizons as a result of we count on you to totally liquidate your funding on the supposed date. With Retirement objectives, we count on you to take distributions over time so we’ll suggest remaining at a better danger allocation at the same time as you attain the goal date.

Auto-adjust is out there in investing objectives with an related time horizon (excluding Emergency Fund objectives, the BlackRock Goal Earnings portfolio, and the Goldman Sachs Tax-Sensible Bonds portfolio) for the Betterment Core portfolio, SRI portfolios, Innovation Expertise portfolio, Worth Tilt portfolio, and Goldman Sachs Sensible Beta portfolio. If you need Betterment to mechanically modify your investments based on these glidepaths, you’ve the choice to allow Betterment’s auto-adjust characteristic while you settle for Betterment’s really helpful allocation. This characteristic makes use of money movement rebalancing and promote/purchase rebalancing to assist preserve your objective’s allocation inline with our really helpful allocation.

Adjusting for Threat Tolerance

The above funding allocation suggestions and glidepaths are based mostly on what we name “danger capability” or the extent to which a shopper’s objective can maintain a monetary setback based mostly on its anticipated time horizon and liquidation technique. Shoppers have the choice to agree with this advice or to deviate from it.

Betterment makes use of an interactive slider that permits purchasers to toggle between totally different funding allocations (how a lot is allotted to shares versus bonds) till they discover the allocation that has the anticipated vary of progress outcomes they’re prepared to expertise for that objective given their tolerance for danger. Betterment’s slider accommodates 5 classes of danger tolerance:

- Very Conservative: This danger setting is related to an allocation that’s greater than 7 share factors beneath our really helpful allocation to shares. That’s okay, so long as you’re conscious that you could be sacrifice potential returns with a view to restrict your chance of experiencing losses. It’s possible you’ll want to avoid wasting extra with a view to attain your objectives. This setting is acceptable for individuals who have a decrease tolerance for danger.

- Conservative: This danger setting is related to an allocation that’s between 4-7 share factors beneath our really helpful allocation to shares. That’s okay, so long as you’re conscious that you could be sacrifice potential returns with a view to restrict your chance of experiencing losses. It’s possible you’ll want to avoid wasting extra with a view to attain your objectives. This setting is acceptable for individuals who have a decrease tolerance for danger.

- Reasonable: This danger setting is related to an allocation that’s inside 3 share factors of our really helpful allocation to shares.

- Aggressive: This danger setting is related to an allocation that’s between 4-7 share factors above our really helpful allocation to shares. This provides the good thing about probably greater returns within the long-term however exposes you to greater potential losses within the short-term. This setting is acceptable for individuals who have a better tolerance for danger.

- Very Aggressive: This danger setting is related to an allocation that’s greater than 7 share factors above our really helpful allocation to shares. This provides the good thing about probably greater returns within the long-term however exposes you to greater potential losses within the short-term. This setting is acceptable for individuals who have a better tolerance for danger.