{kind=link}

Taxes. You could strive to think about them as little as potential, however they’re on our minds loads. Particularly after they relate to investments. That’s as a result of we’re all the time seeking to maximize our prospects’ potential take-home returns—and key to that pursuit is minimizing how huge of a chew taxes take.

On that entrance, our Tax Coordination function is a fully-automated method to an funding technique often called asset location—and it’s accessible at no further value. When you’re saving for retirement in a couple of kind of account, then asset location normally, and our spin on it particularly, may help to extend your after-tax anticipated returns with out taking up further threat. Right here’s how.

How Tax Coordination works

Many Individuals wind up saving for retirement in some mixture of three account sorts:

- Taxable

- Tax-deferred (Conventional 401(okay) or IRA)

- Tax-exempt (Roth 401(okay) or Roth IRA)

Every kind of account will get a unique tax remedy, and completely different property are taxed otherwise as nicely. These guidelines make sure investments a greater match for one account kind over one other.

Returns in IRAs and 401(okay)s, for instance, don’t get taxed yearly, so they typically shelter development from tax higher than a taxable account. We’d moderately defend property that lose extra to tax in a majority of these retirement accounts, property reminiscent of bonds, whose dividends are normally taxed yearly and at a excessive price.

Within the taxable account, nonetheless, we’d typically want to have property that don’t get taxed as a lot, property reminiscent of shares, whose development in worth (“capital good points”) is taxed at a decrease price and crucially solely after they’re “realized,” or in different phrases, after they’re bought at the next worth than what you paid for them.

Properly making use of this technique to a globally-diversified portfolio can get sophisticated shortly. Try our full Asset Location methodology in the event you’re curious what that complexity appears to be like like—or hold studying for extra of the simplified clarification.

The large image diversification of asset location

When investing in a couple of account, many individuals choose the identical portfolio in every one. That is straightforward to do, and if you add every thing up, you get the identical portfolio, solely larger.

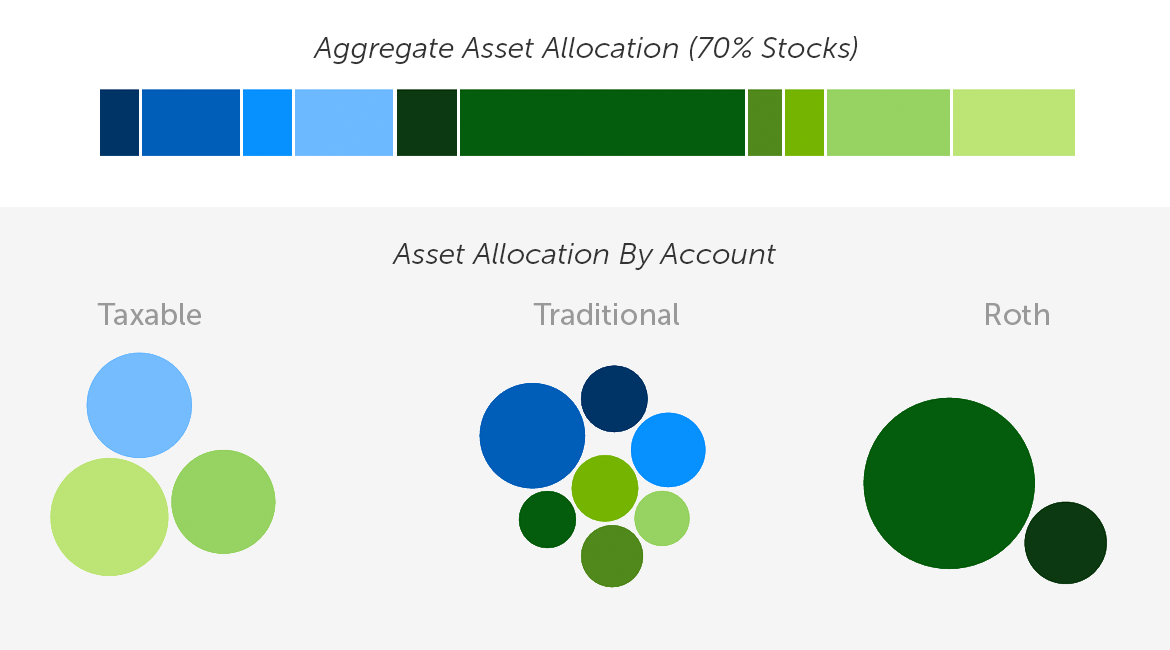

As an instance this method, right here’s what it appears to be like like with a hypothetical asset allocation of 70% shares and 30% bonds. The completely different shades of inexperienced characterize varied varieties of shares, and the completely different shades of blue characterize varied varieties of bonds.

However so long as all of the accounts add as much as the portfolio we would like, every particular person account by itself doesn’t must mirror that portfolio. Every asset can go within the account the place it makes essentially the most sense from a tax perspective. So long as we nonetheless have the identical portfolio once we add up the accounts, we are able to improve the after-tax anticipated return with out taking up extra threat. That is asset location in motion, and right here’s what it appears to be like like, once more for illustrative functions:

This is similar general portfolio as we initially confirmed, besides we redistributed the property erratically to cut back taxes. Notice that the combination allocation remains to be a 70/30 break up of shares and bonds.

The idea of asset location isn’t new. Advisors and complex do-it-yourself traders have been implementing some model of this technique for years. However squeezing it for extra profit could be very mathematically-complex. It means making vital changes alongside the way in which, particularly after making deposits to any of the accounts. Our expert-built expertise handles all the complexity in a means {that a} handbook method simply can’t match.

Our rigorous analysis and testing, as outlined in our Asset Location methodology, demonstrates that accounts managed by Tax Coordination are anticipated to yield meaningfully increased after-tax returns than uncoordinated accounts.

The best way to profit from Betterment’s Tax Coordination

To profit from from our Tax Coordination function, you first must be a Betterment buyer with a steadiness in no less than two of the next varieties of Betterment accounts:

- Taxable account

- Tax-deferred account: A Conventional IRA or a Betterment Conventional 401(okay) supplied by your employer.

- Tax-exempt account: A Roth IRA or a Betterment Roth 401(okay) supplied by your employer.

Notice you can solely embody a 401(okay) in a objective utilizing Tax Coordination if it’s one we handle on behalf of your present or former employer. In case your employer doesn’t presently use Betterment to offer their 401(okay) plan, inform them to offer us a take a look at betterment.com/work!

You probably have an previous 401(okay) with a earlier employer, you’ll be able to nonetheless profit from our Tax Coordination function by rolling it over to a Betterment IRA.

For step-by-step directions on the best way to arrange Tax Coordination in your Betterment account, in addition to solutions to steadily requested questions, head on over to our Assist Middle. Or in the event you’re not but a Betterment buyer, get began by signing up at this time.